Latest articles on Life Insurance, Non-life Insurance, Mutual Funds, Bonds, Small Saving Schemes and Personal Finance to help you make well-informed money decisions.

While a term life insurance plan protects your financial dependants in case you die, a health insurance is a must for every individual given the rising incidence of ailments and high medical costs

You may not be as fit in your 50s as you were in your 20s. That’s a fact of life: as you grow older, your body shows signs of wear and tear and you need more medical care than before, worse lifestyle choices make you susceptible to life altering ailments that can also cost a bomb.

Research shows that heart ailments and cancer account for over half of casualties among Indians. In fact, India has the highest rate of cardiac arrests in the world and every 13th new cancer patient is from India, research suggests. If the facts disturb you and you don’t have adequate life and health insurance plan, you should indeed be worried.

A health insurance policy pays for your hospital bills and life insurance provides timely financial support to your loved ones after you die. Both are important covers to have and we tell you who needs these policies, how much and how often one needs to review the cover.

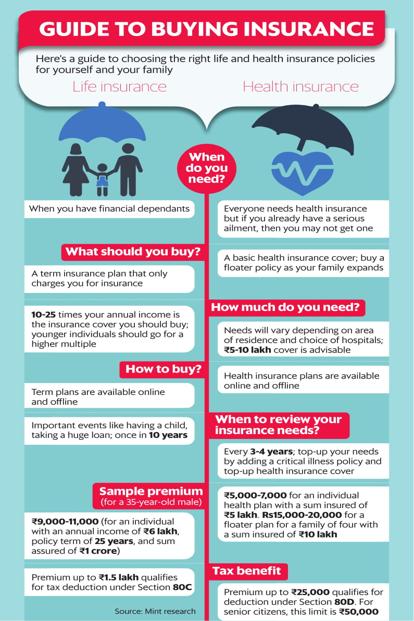

LIFE COVER

Who needs it and when? Not everyone needs life insurance. Children and young adults who are not working and retired individuals come under this category and that’s because they don’t have anyone depending on them financially. If you are not working, you are not providing for anyone. Similarly in your sunset years, your children are working and you have amassed enough assets to fall back on.

It’s the sandwich generation—the working class that provides for children and often older parents—that needs life insurance; in fact buying life insurance needs to be a priority for this generation. Mint Money recommends buying a term insurance cover, but how much should you buy? Life insurance plans are typically level term policies, which means you pay the same premium for life.

How much cover do you need? According to KS Gopalakrishnan, CEO, RGA (Canada-based reinsurance firm), India, the younger you are, the higher cover you need. “The thumb rule says 10 times the annual income, but the actual need could be between 10 and 25 times,” said Gopalakrishnan.

“Younger individuals don’t have enough assets to fall back on. They have more number of working years ahead and liabilities only increase in terms of expanding family and big ticket loans. A higher multiple therefore works, as they can get it at a cheaper cost and don’t have to keep reviewing and buying more insurance policies,” he added.

A cover of 10-25 times your salary may look huge to you now, but if you factor in the time value of money, you will realise it won’t be all that big many years down the line. “If you are a salaried individual, insurers can give a cover up to 20 times your annual income. So, opt for a higher cover early on. Then you need not review your life cover often. A relook is needed when you have a baby or once in 10 years,”said Kapil Mehta, co-founder, SecureNow.in.

“For a large loan you could take a separate term plan. But other than this, you don’t need multiple policies. Also, given that premium for term plans have fallen in recent times, it may make sense to review your insurance and buy a new plan and then lapse your older, more expensive plan,” added Mehta.

HEALTH COVER

Why do you need it? Everyone needs health insurance and that’s because the cost of medical treatment is high. “While ailments may not be much of a concern for young people, accidents can still happen. They need health insurance to financially protect themselves against hospitalization due to accidents or even infection,” said Jyoti Punja, chief customer officer, Cigna TTK Health Insurance Co. Ltd.

Such cases of hospitalization can work up a neat bill. For instance, dislocation, sprain and strain of joints and ligaments that needs surgical intervention or fracture of the leg needing surgery can cost up to ₹4 lakh in metro cities and up to ₹2 lakh in non-metros.

Which plan should you buy? If you are single and working, you can start with an individual policy. Once you get married, increase the cover by buying a floater policy. “A floater policy works best for a family in the same age group. But if there is a large age gap between the spouses or if parents need health insurance as well or if a family member suffers from ailments like diabetes, then individual insurances for these members may be better”added Mehta. Infants and young children can be added to a floater policy.

How much cover do you need? A health insurance policy is a must but it’s equally important to understand how much you need to buy. It’s also important to get this right because as you grow older you may contract ailments and then it’s an uphill task to get insured. It’s always a good idea to have your own health policy but how much will depend on various factors.

“You need to first understand the type of hospitals you would visit. Today, in a corporate hospital in a metro, treatment for a heart attack can cost upwards of ₹10 lakh. That’s the minimum you need. This amount will increase over time so you need to review your health insurance sum assured every 3-5 years,” added Mehta.

For senior citizens, individual plans may work best.

How to increase your cover? You can increase your health insurance by buying a top-up plan that comes with a deductible. Read more about it here. It’s important to have a decent base cover because that way a top-up plan can be very cost effective.

Other than this, you can also buy a critical illness policy that pays a lump sum on diagnosis of a critical illness such as cancer. This policy works to supplement your income. But remember a health policy doesn’t pay for the entire cost of hospitalisation, so your emergency fund needs to have a corpus for medical emergencies.

Money management is important, but it’s not limited to savings and investments alone, buying the right kind of insurance is an important step to that end.

Copyright © 2025 Design and developed by Fintso. All Rights Reserved

Industry News

Industry News